The Gulf Cooperation Council (GCC) nations—Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman—are at a pivotal moment in their energy journey. Historically reliant on oil and gas exports, these countries have benefited immensely from hydrocarbons, which have powered their economies and enabled massive infrastructure development. However, with global markets shifting towards renewable energy to address climate change, the GCC must navigate a complex transition: how to retain its dominant role in oil while embracing clean energy technologies that will define the future.

Oil’s Central Role and the Coming Shift

Oil has long been the foundation of GCC economies. In Saudi Arabia, the world’s largest oil exporter, oil accounts for around 50% of GDP and 70% of export earnings. Similarly, in Kuwait and Qatar, oil revenues are crucial to their national budgets. This reliance on hydrocarbons has allowed these nations to prosper, but it has also created economic vulnerabilities. Global efforts to reduce carbon emissions are pressuring oil-dependent economies to diversify.

The world is now in the midst of an energy transition, with renewable energy sources like solar, wind, and green hydrogen gaining traction. The International Energy Agency (IEA) predicts that global demand for oil will peak within the next decade. For the GCC, this raises an existential question: how quickly can they adapt to this new reality? While they benefit from some of the lowest oil production costs in the world, staying competitive means finding ways to diversify before demand for their primary export declines.

Renewables: Bold Ambitions

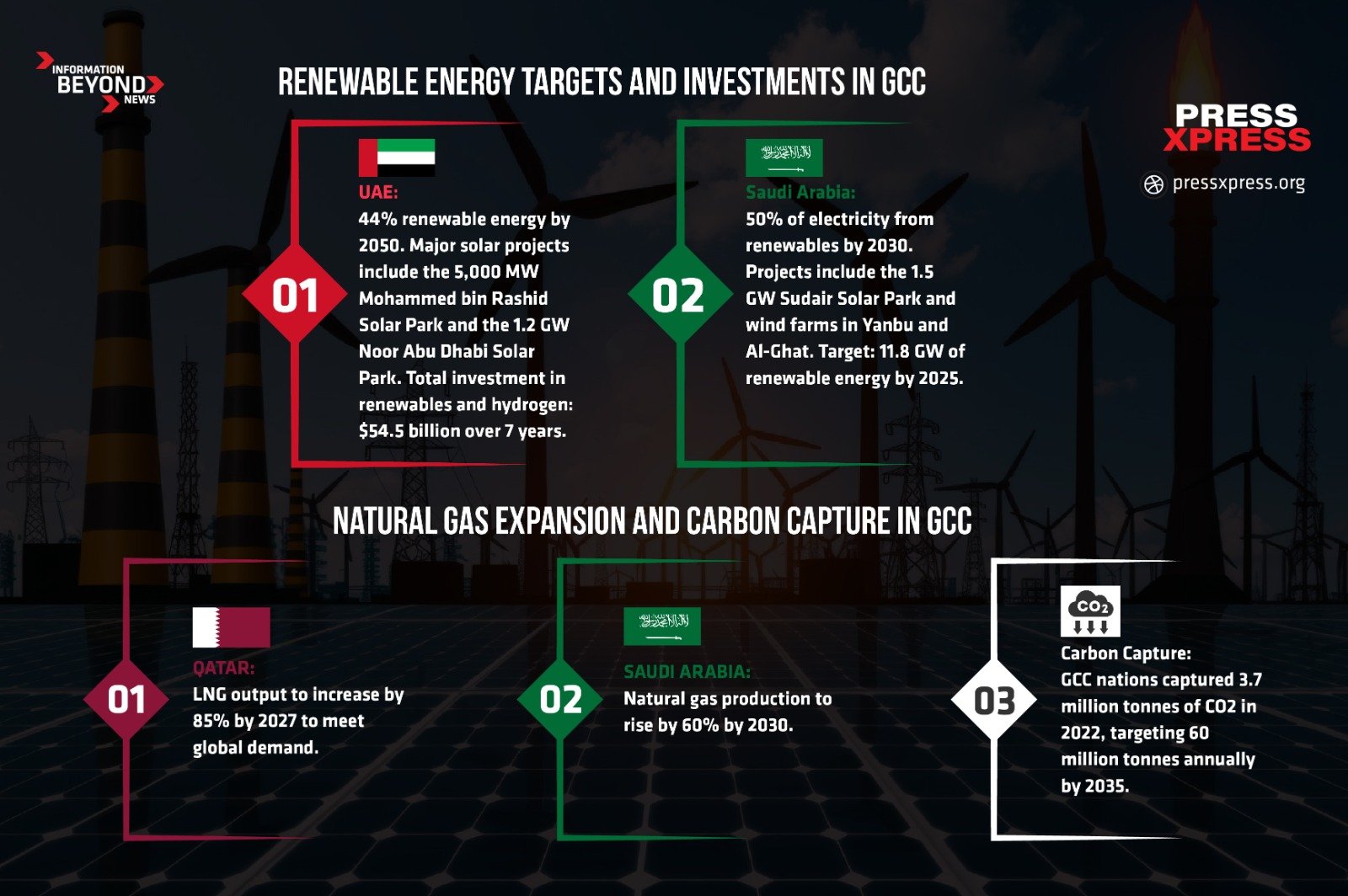

The GCC has recognized the need for change. Countries like the UAE and Saudi Arabia have announced ambitious renewable energy targets. The UAE, for example, aims to have 44% of its energy mix come from renewables by 2050. Projects such as the Mohammed bin Rashid Al Maktoum Solar Park, one of the world’s largest, are key to this strategy. Saudi Arabia, meanwhile, aims for 50% of its electricity to come from renewable sources by 2030. These targets reflect a clear understanding of the need to transition, but the path forward is not without challenges.

While the region is rich in sunlight and has vast tracts of land ideal for solar power, building out the necessary infrastructure at scale will take time and investment. Moreover, renewable energy projects are capital-intensive and require significant upfront investment, which may strain government budgets still heavily reliant on oil revenues.

Green Hydrogen: The Next Big Bet

Green hydrogen has emerged as one of the most promising areas for future energy development in the GCC. Produced using renewable energy sources, green hydrogen is seen as a solution for decarbonizing sectors that are difficult to electrify, such as heavy industry and transportation.

Saudi Arabia has taken a bold step with its $8.4 billion NEOM project, which aims to produce 600 tonnes of green hydrogen per day by 2026. This project could position the Kingdom as a leader in the global hydrogen market. Oman has also announced plans to become a major player, with targets to produce 7.5 million tonnes of green hydrogen annually by 2050. The UAE is following suit, investing $54.5 billion over the next seven years in hydrogen development.

However, the commercial viability of green hydrogen remains a challenge. The technology is still in its early stages, and producing green hydrogen at scale is expensive. Developing a global market for hydrogen will require both investment in production capacity and the creation of demand, especially in regions like Europe and Asia, which are pushing for cleaner energy sources.

Natural Gas: The Bridge to Renewables

Despite the focus on renewables, natural gas remains a critical part of the GCC’s energy strategy. Qatar, the world’s largest exporter of liquefied natural gas (LNG), is increasing its output by 85% by 2027 to meet growing global demand. Saudi Arabia is similarly expanding its natural gas production by 60% by 2030.

Natural gas is seen as a “bridge fuel” for the transition to cleaner energy. While it emits fewer carbon emissions than oil or coal, it is still a fossil fuel, and its role in the long-term energy mix remains a subject of debate. For the GCC, natural gas offers a way to continue their leadership in global energy markets while supporting the growth of renewables.

Carbon Capture: A Key Technology for Oil’s Future

As the GCC explores renewable energy, it is also investing in technologies to reduce the environmental impact of continued oil and gas production. Carbon Capture, Utilization, and Storage (CCUS) has become a critical tool in this effort. In 2022, GCC countries captured 3.7 million tonnes of CO2, representing 10% of global carbon capture efforts. By 2035, they aim to capture 60 million tonnes annually.

Saudi Arabia has launched a regional carbon credit trading platform, and both the UAE and Qatar are leading efforts to scale up carbon capture technologies. However, critics argue that relying on CCUS could slow the transition to renewable energy by allowing countries to continue producing oil under the guise of reducing emissions.

Economic Diversification: A Tough Road Ahead

Despite these renewable energy initiatives, the GCC still faces a significant challenge in reducing its economic reliance on hydrocarbons. In countries like Qatar and Kuwait, oil and gas still make up over 60% of government revenues. Economic diversification has long been a goal for the region, but progress has been slow. The private sector remains underdeveloped, and many non-oil industries have struggled to gain traction.

Nonetheless, renewable energy offers a potential path forward. If the GCC can leverage its investments in green hydrogen, solar power, and other clean technologies, it could reduce its dependence on oil while tapping into the growing global demand for clean energy solutions.

The Road Ahead: Can the GCC Strike a Balance?

The GCC nations are clearly working to diversify their energy portfolios, but the transition is complex and fraught with challenges. Their economies remain deeply intertwined with the global oil market, and moving toward a renewable future will require a careful balancing act. Investments in solar power, green hydrogen, and carbon capture technologies show that the GCC is serious about its energy transition, but whether these efforts can outpace the decline in global oil demand remains to be seen. The next decade will be crucial. The GCC’s ability to navigate this energy transition while maintaining economic stability will determine its future role in global energy markets. Whether they can lead both in oil and renewables remains an open question, but their actions today will shape the region’s trajectory for years to come.