Key Highlights:

- US inflation cooled in the summer of 2022, while it continued rising in Europe.

- In 2022, around 22% of the EU’s imports came from China, a figure that has increased in recent years.

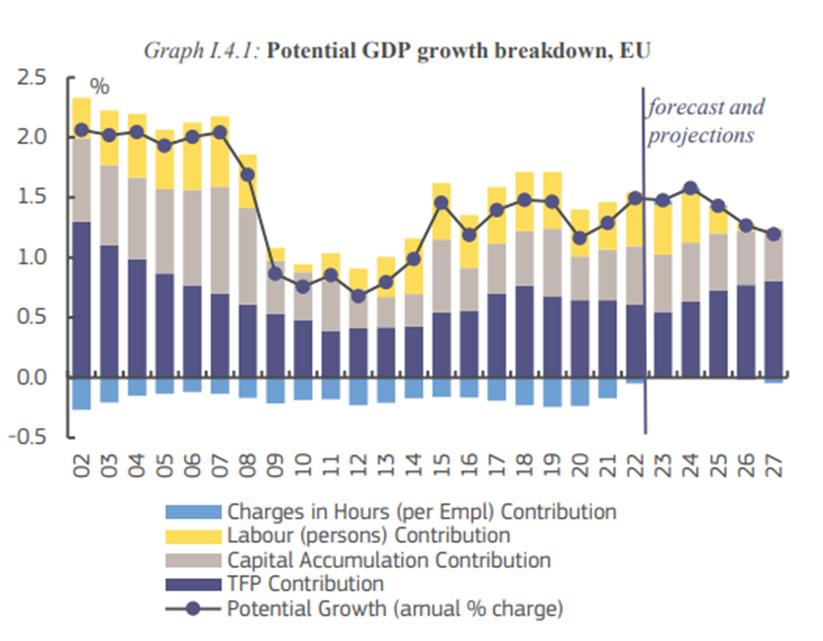

- The European Commission predicts the bloc’s growth to dip below 1.5%, further declining to 1.2% by 2027 from the previous 2%-2.5%

The old world has new problems, indeed, throughout 2023, the European economy experienced nearly zero growth. Germany and the UK, the continent’s largest economies, are both potentially slipping into recession. Leading European firms like Volkswagen, Nokia, and Union Bank of Switzerland have collectively announced massive layoffs. In Paris, angry farmers are blocking major roads, while tens of thousands of German transport workers recently went on strike.

You can also read: Donald Trump Survives Assassination Attempt!

These domestic issues are reverberating in Europe’s geopolitical landscape. In crucial areas like energy and innovation, Europe finds itself outmaneuvered by the US and China.

Building a resilient Europe capable of shaping its future is paramount at this moment. The pandemic, geopolitical instability, conflict, and climate crisis have shattered the sense of security and stability Europe once enjoyed. Now, these challenges demand proactive solutions rather than assumptions of security and resilience.

How the US Outspent Europe?

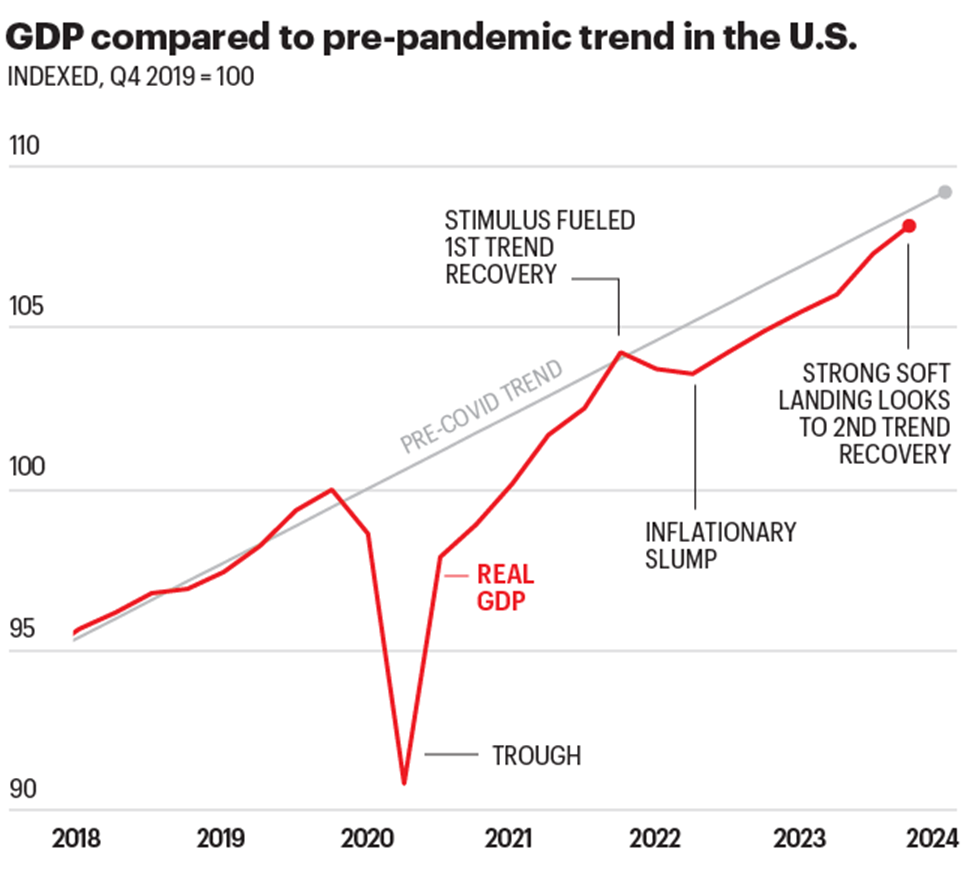

More than eighteen months ago, economists predicted a recession due to the pandemic, inflation, and energy crisis in both Europe and the US. Instead, the US economy is thriving while Europe struggles. The US achieved this by adopting Europe’s big-government approach but executing it better.

In March 2020, governments worldwide increased spending. The UK and Germany spent over $500 billion, France $235 billion, and Italy $216 billion. The US, however, spent an unprecedented $5 trillion on pandemic relief—more than the New Deal and World War II combined and double what European countries spent relative to their economies.

US inflation cooled in the summer of 2022 while it continued rising in Europe. Americans had about $2.5 trillion in excess savings, bolstering them against economic challenges.

Europe supported workers by paying employers, while the US expanded unemployment insurance. The $800 billion Paycheck Protection Program was largely ineffective.

Post-pandemic, the US invested over $2 trillion in infrastructure, manufacturing, and clean energy through various acts. While interest rate increases typically hamper debt-dependent sectors like construction and manufacturing, these industries are booming in America. Companies have announced about $650 billion in investments since 2021, and private investment in manufacturing facilities reached its highest level since 1958 last year.

The US-Europe economic gap widened in 2023 after the worst of the energy crisis. America’s aggressive spending was possible due to its unique position. Since 2019, the US has added more than $10 trillion to the national debt, with a $1.7 trillion deficit in 2023—a level of spending unthinkable for European leaders.

China Surges Ahead of Europe in Clean Energy Innovation

China has surpassed Europe in clean-energy technologies. In 2021, China led several peer-reviewed publications in fields like solar and wind power, lithium batteries, heat pumps, and carbon capture technology. This marks a significant shift from 2010, when the EU led in all these sectors except wind.

European Commission President Ursula von der Leyen has advocated for a strategy of “de-risking” from China, aiming to reduce dependencies on critical technologies, including solar cells. While Europe’s reliance on China for products like solar cells is well documented, the widening gap in research and innovation could hinder the EU’s efforts to decrease these dependencies.

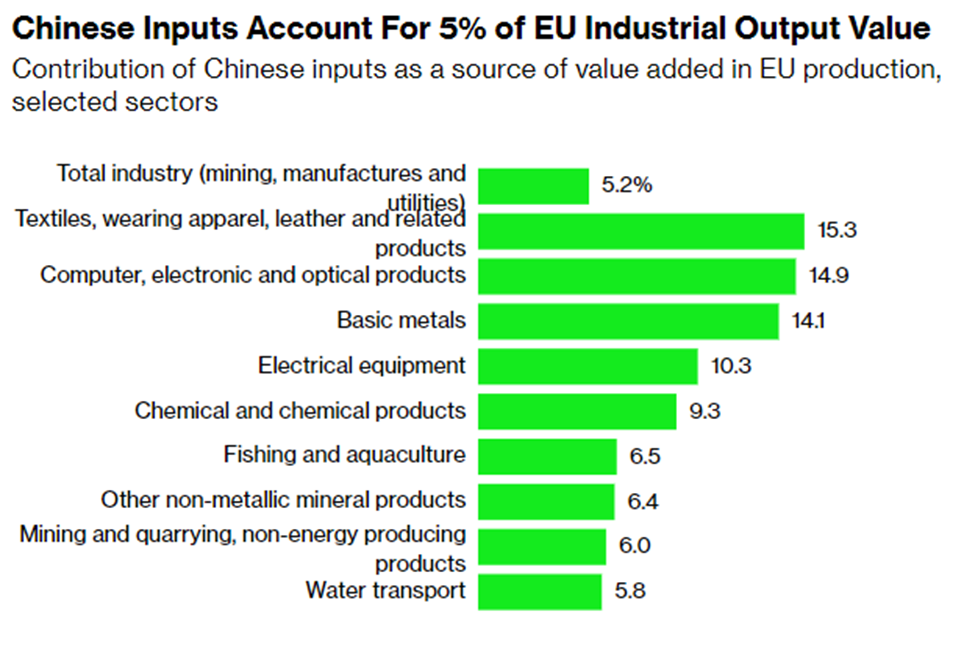

In 2022, around 22% of the EU’s imports came from China, a figure that has increased in recent years even as the equivalent figure for the US has declined. EU industries such as basic metals, chemicals, electronics, and electrical equipment are particularly dependent on Chinese inputs across international supply chains.

Europe’s Economic Fall from Grace

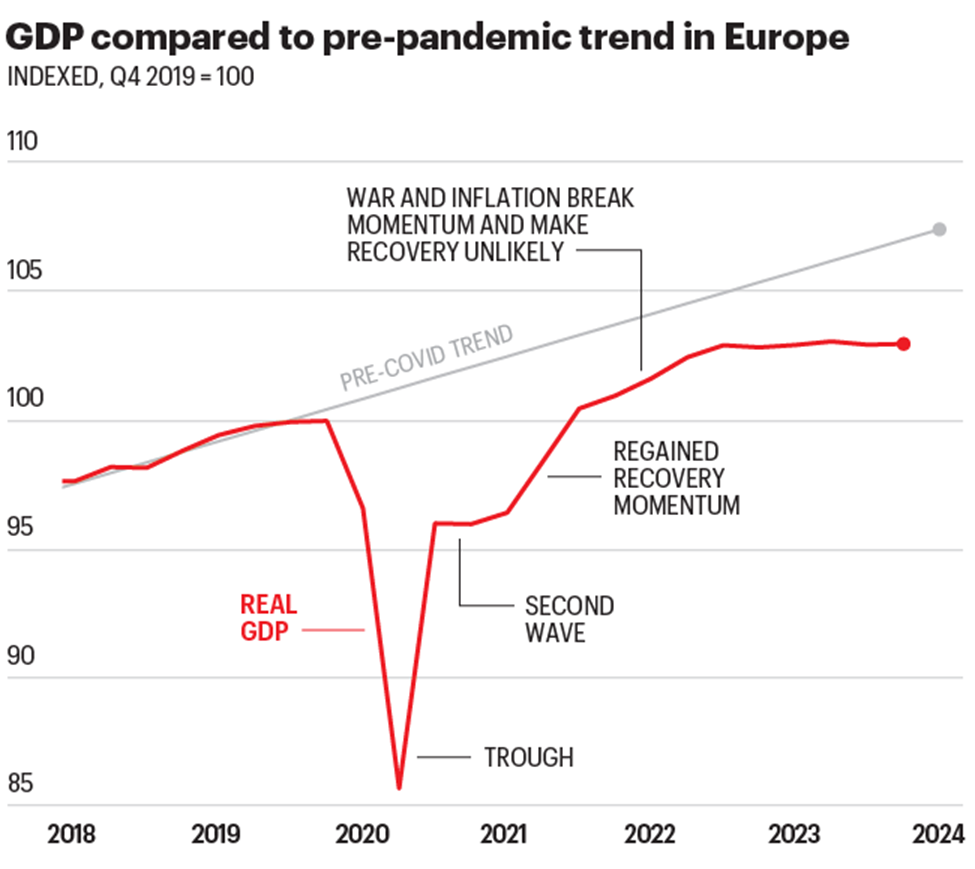

Over the past year, European countries have slashed budgets to address pressing economic needs, leading to public outrage, protests, and a rise in far-right political factions. The European Commission predicts the bloc’s growth to dip below 1.5%, further declining to 1.2% by 2027 from the previous 2%-2.5%, due to demographic changes and stagnant productivity.

This continues a bleak economic trend: the eurozone has seen no significant growth since the third quarter of 2022, with only a 0.5% increase. Early 2024 indicators still show contraction. Additionally, disruptions in the Red Sea have increased shipping costs and threaten inflation.

French farmers, demanding better pay and fewer constraints, have blockaded Paris. The European Central Bank’s (ECB) anti-inflation measures — higher interest rates — have dampened business investment and real estate activities.

Germany, Europe’s largest economy, contracted by 0.3% in the fourth quarter, struggling with higher fuel prices after Russia cut off natural gas, a shortage of skilled workers, and years of underinvestment in infrastructure and digital technology.

Some analysts expect the ECB to cut interest rates, while others believe the central bank may wait to ensure inflation is controlled. Risks remain, including attacks by Yemen’s Houthi rebels on ships in the Red Sea amid Israel’s war on Hamas, potentially adding 0.5% to core inflation, according to Oxford Economics.

Can Europe Catch Up to the US and China?

European companies like Maersk are investing heavily in new technologies to accelerate the green transition. Europe must also play a key role globally by pushing for mechanisms like the International Maritime Organization’s price scheme, which would charge fossil fuel emitters extra while subsidizing green fuel users.

Although Europe has been a hub for innovation, US productivity growth and investment in research have outpaced Europe’s, driven by Silicon Valley and a robust start-up ecosystem. Meanwhile, China is investing massively in AI, 5G, and quantum computing.

Despite Europe’s rich scientific history, it faces challenges due to bureaucracy and restrictive regulations. To achieve ‘open strategic autonomy,’ Europe must boost funding and incentives for research and development, create attractive investment conditions, and strengthen the single market by removing internal trade barriers and enhancing integration.

Moving from a defensive regulatory stance to fostering competitive companies is crucial. Addressing bureaucratic obstacles is essential to avoid legislation that disadvantages businesses and discourages investment.

Europe is not yet in check, let alone checkmate, but its lack of determination leaves it vulnerable. To avoid this, Europe must consolidate its strengths, streamline regulations, deepen integration, and invest boldly. Otherwise, it risks becoming a mere spectator in the high-stakes geopolitical arena.