- A significant shift towards digital payments driven by economic resilience and youth demographic

- Banking companies require Bangladesh Bank approval for payment system participation.

In a significant stride towards modernizing its financial infrastructure, the Bangladesh Parliament has passed the ‘Payment and Settlement System Bill, 2024’. This comprehensive legislation introduces a robust legal framework governing both bank and non-bank payment services, addressing critical regulatory gaps in the country’s dynamic financial sector.

Finance Minister A H Mahmood Ali, presenting the bill to the Jatiya Sangsad, highlighted its pivotal role in safeguarding consumer interests. “This bill fills a longstanding void in Bangladesh’s financial regulations,” Ali emphasized. “It ensures greater security and accountability for all financial transactions, which were previously unregulated.”

You can also read: Understanding Aging In Rural Bangladesh

Under the new law, all payment services are now under the direct supervision of Bangladesh Bank, marking a pivotal shift towards enhanced oversight and standardization across diverse payment platforms, from traditional banking channels to emerging fintech solutions.

What are the Objectives of the ‘Payment and Settlement System Bill-2024’?

The bill’s Statement of Purpose and Reasons underscores the significant gap in Bangladesh’s financial regulatory framework. Currently, the country lacks dedicated legislation governing payment and settlement systems, relying instead on outdated laws like the Bangladesh Bank Order-1972 and Regulations on Electronic Fund Transfer-2014. This regulatory vacuum has necessitated an ad hoc arrangement where banks operated under contractual obligations with Bangladesh Bank, lacking a unified legal framework to oversee non-bank financial institutions’ payment activities.

The proposed legislation aims to rectify these deficiencies by establishing a unified legal structure that encompasses both traditional banking institutions and emerging non-bank payment service providers. This comprehensive approach aims to enhance customer protection in an increasingly diverse and complex financial services landscape.

Key Provisions and Regulatory Measures

The bill introduces crucial provisions to effectively regulate the payment landscape. Banking companies must now obtain Bangladesh Bank’s approval before participating in any payment system, operating payment systems, or providing electronic currency payment services. The issuance, acquisition, and trading of ‘Prepaid Payment Instruments’ also require Bangladesh Bank’s authorization. Moreover, the legislation prohibits any unauthorized online or offline financial activities, ensuring a comprehensive regulatory framework for all financial transactions.

Digital Payment Revolution in Bangladesh

Over the past decade, Bangladesh has witnessed a significant shift towards digital payments, driven by evolving consumer behavior and accelerated by the COVID-19 pandemic. The country’s economic resilience, burgeoning middle class, and youthful demographic (62% under 30) have been pivotal in driving this transformation.

Key milestones include a 57% increase in financial inclusion from 2013 to 2018, alongside a 31.5% rise in internet penetration by early 2022. Mobile Financial Service (MFS) transactions recorded a 7% growth in Q3 FY 2019-20, indicating growing acceptance of digital financial solutions.

Government initiatives in digitalization and the rise of online businesses have further diversified payment systems, positioning Bangladesh’s digital payment landscape for continued innovation and growth.

Growth Trajectories and Challenges

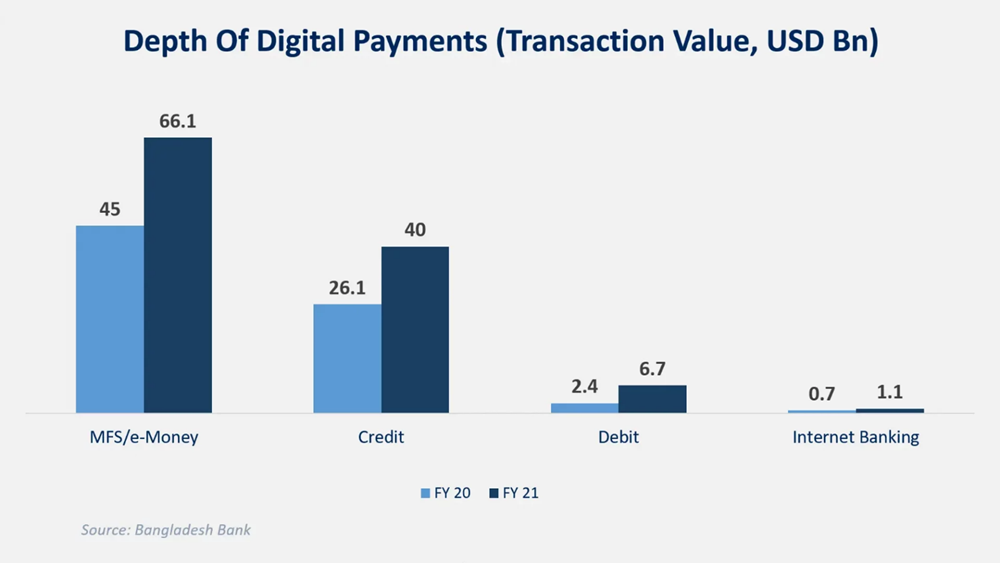

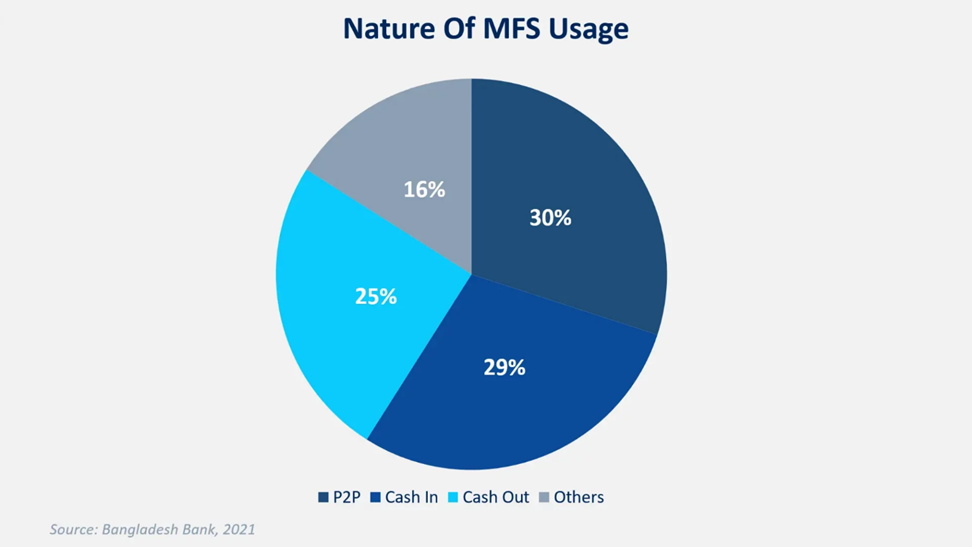

Bangladesh’s digital financial services sector has seen remarkable growth, with the ecosystem now boasting over 170 million accounts across banks, Non-Bank Financial Institutions (NBFIs), Mobile Financial Services (MFS), Micro-Finance Institutions (MFIs), and Fintech companies. Notably, MFS users surged by 159% from 2018 to 2021, reflecting strong adoption of digital financial solutions.

Despite these achievements, challenges remain. Approximately 30 million Bangladeshis remain unbanked, hindering financial access among lower-income groups. However, initiatives through MFIs, MFS, and agent banking have contributed to a 30% increase in financial inclusion for the underbanked in the fiscal year 2021, highlighting the transformative potential of digital solutions in fostering financial inclusivity.

Guidelines for Prepaid Instruments and Digital Infrastructure

The bill also outlines guidelines for issuing Prepaid Instruments (PIs), defining their classifications and scope. These instruments play a crucial role in enabling digital payments, subject to stringent regulations to ensure security and integrity.

Barriers and Penalties

Despite new opportunities in the payment system, significant obstacles persist:

- MFS Frauds: One in ten MFS users in Bangladesh has experienced financial fraud, according to a PRI survey. These scams undermine trust in MFS providers, prompting users to revert to traditional payment methods.

- Lack of Financial Literacy: Over 60% of MFS users rely on others to manage their accounts, compromising data privacy and security, as highlighted by a BIGD survey. This lack of understanding contributes to fraud incidents.

- Limited Access to Digital Payments: Accessibility to formal digital payments is constrained, especially in rural areas where ATMs and POS terminals are scarce. Perceived complexities and distrust hinder the adoption of credit cards and digital payment methods nationwide.

- Inadequate Digital Infrastructure: Only 41% of mobile users in Bangladesh owned smartphones as of 2020, compounded by poor internet connectivity in rural regions. This digital divide restricts access to essential digital financial services for many.

Penalties for Non-Compliance

To ensure strict adherence to the new regulations, the bill outlines severe penalties for violations. Individuals found guilty of contravening the provisions may face imprisonment for up to five years, a fine of up to Tk 5 million, or both. The law also addresses the issue of false information, imposing penalties of up to three years imprisonment or a fine of Tk 3 million for furnishing inaccurate details in statements, reports, or other documents. These stringent measures aim to deter fraudulent activities and promote transparency in the financial sector.

Opposition Concerns and Amendments

During the discussion, opposition and independent lawmakers expressed concerns about the current state of the banking system, attributing issues to a lack of rule enforcement. However, amendment proposals from opposition lawmakers were rejected through voice votes.