India’s central bank is expected to reassess its foreign exchange strategy in 2025, loosening its grip on the rupee as the currency remains at its strongest trade-weighted level in two decades, according to economists.

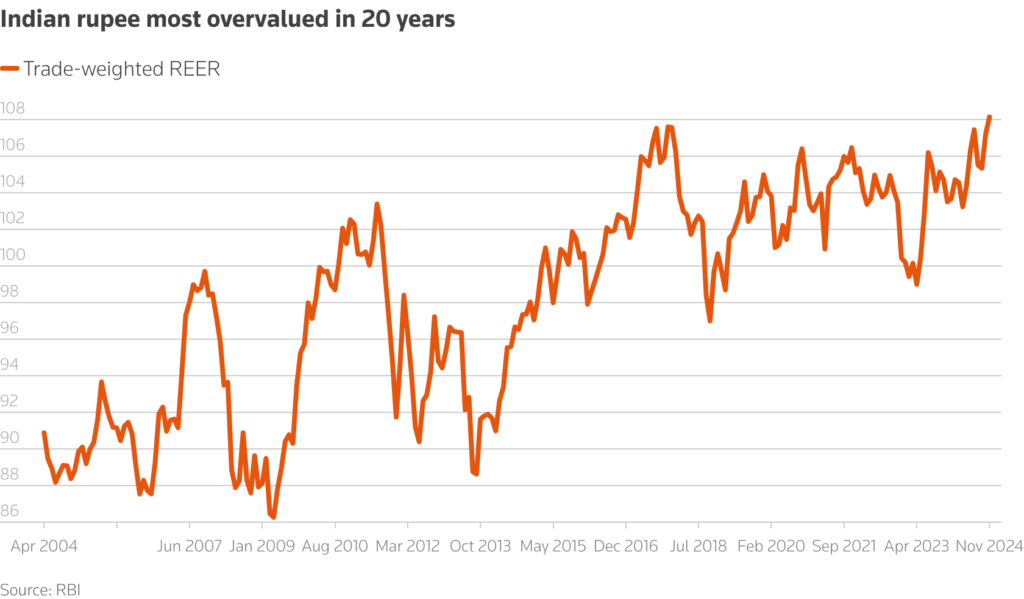

The rupee’s 40-currency trade-weighted real effective exchange rate (REER) stood at 108.14 in November, suggesting an overvaluation of about 8%, as per the Reserve Bank of India’s (RBI) latest bulletin. This marks the highest overvaluation since 2004, the earliest year for which RBI data is available.

Impact of Overvaluation

The rupee’s overvaluation makes Indian exports more expensive relative to trading partners, which can hurt the country’s export competitiveness. Economists attribute this overvaluation to the currency’s nominal appreciation against its peers and widening interest rate differentials.

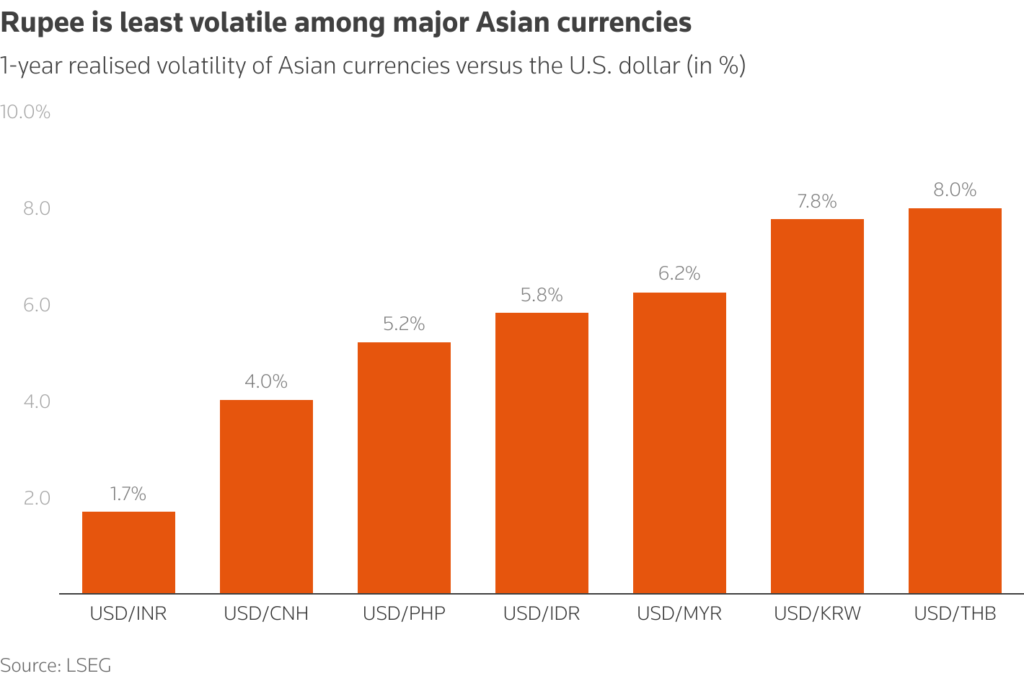

This strength is largely a result of frequent RBI interventions in the forex market aimed at curbing the rupee’s decline and maintaining low volatility. As a result, the rupee has been the least volatile Asian currency this year after Hong Kong’s pegged dollar.

Shift in 2025

Economists anticipate a shift in strategy as the rupee’s overvaluation rises. “Given the rise in rupee’s overvaluation, the pace of RBI forex intervention will need to slow,” said Gaura Sen Gupta, India economist at IDFC FIRST Bank. This would likely lead to a weaker rupee and increased volatility.

Signs of this adjustment are already visible. The rupee’s 30-day daily realized volatility has reached a six-month high, and it is set to post its largest monthly decline in two years, dropping 1.2% in December. Last Friday, the rupee hit a record low of 85.8075 against the U.S. dollar, trading in a 50-paisa range—the widest this year.

Kanika Pasricha, Chief Economic Advisor at Union Bank of India, noted that the rupee’s “flagging” overvaluation indicates further depreciation may be on the horizon.

Headwinds for the Rupee

The rupee faces multiple challenges in 2025, including a shallow rate-cut cycle by the U.S. Federal Reserve, concerns about the impact of Donald Trump’s trade policies, rising U.S. bond yields, and India’s slowing economic growth.

“It is after several years that both ‘pull’ (growth slowdown) and ‘push’ factors (external headwinds) for portfolio flows are unfavorable for the rupee,” said Dhiraj Nim, economist and FX rates strategist at ANZ. “An adjustment is warranted.”

New Leadership at the RBI

The appointment of Sanjay Malhotra as the new RBI governor earlier this month has further fueled expectations of a shift in the central bank’s currency management approach.

“The RBI governor plays a key role in shaping the central bank’s strategy,” Nomura said in a note following Malhotra’s appointment. “It is possible that more flexibility will be allowed in currency fluctuations moving forward, compared to the tighter control seen over the past year.”

As the central bank navigates these challenges, a recalibrated approach to managing the rupee is likely to emerge, signaling a significant shift in India’s foreign exchange policy.