Key Highlights:

- Summit’s 589 MW power plant received government approval to bypass competitive tenders

- Up to August 2023, the government paid around Tk 1.05 trillion in capacity payments to power plant owners

- Currently, gas-fired power plants account for 10,712MW of the total installed capacity of 25,481MW

Gas-fired power plants account for 10,712MW of Bangladesh’s total installed capacity of 25,481MW, demanding 1,969 million cubic feet per day (mmcfd) of gas. At present, Petrobangla’s total supply is 2,500 mmcfd, of which gas-fired power stations are receiving 700 mmcfd.

In the best-case scenario, Petrobangla can provide 1,000 mmcfd to the power plants from its total supply of 3,500 mmcfd. Despite gas being the cheapest fuel, the country is currently able to produce only around 3,500-4,000MW from gas out of the total generation of 9,500MW to 10,500MW.

You can also read: Bangladesh Sets $110 Billion Export Target

According to Petrobangla’s plans, the gas supply is expected to increase adequately only in 2026, thanks to the drilling of new gas wells and long-term LNG import deals.

3 New Plants Firing Up with Gas Running Low

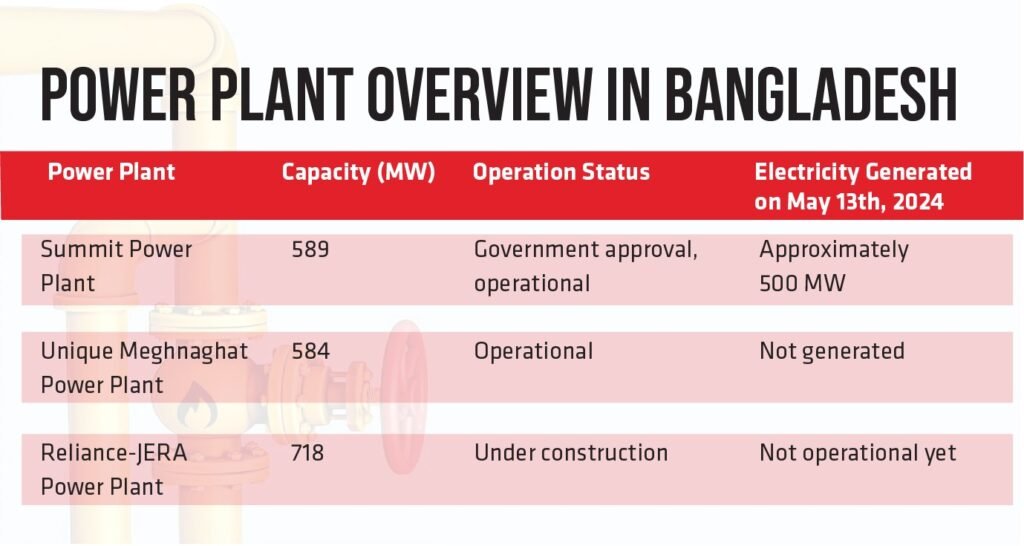

Several new plants are operational or nearing completion, including a 589MW plant by Summit Group that received approval to bypass tenders under the Quick Enhancement of Electricity and Energy Supply (Special Provision) Act 2010. The Bangladesh Power Development Board states this Summit plant generated around 500MW on May 13th.

Another new 584MW plant from Unique Meghnaghat began commercial operations this year, though it did not generate power on May 13th. Nearby, a joint 718MW LNG plant by India’s Reliance Power and Japan’s JERA awaits its commercial operation date to start generating.

Despite these additions, Bangladesh’s total generation during peak evening hours on May 13th was only around 15,019MW out of 26,354MW capacity. Up to August 2023, the government paid around Tk1.05 trillion in capacity payments to power plant owners. With the new plants coming online, this amount is expected to increase further.

Power Grid Delays Cost Bangladesh Billions in Idle Capacity Charges

The state-run Power Grid Company of Bangladesh (PGCB) hasn’t finished constructing 6 substations, causing a bottleneck in evacuating electricity from new plants. These substations won’t be ready before December, so several other LNG-fired plants won’t be able to run even after obtaining their commercial operation dates (CODs).

As a result, BPDB is expected to incur additional costs in capacity payments. According to BPDB annual reports, the average cost per unit of power generation was Tk6.61 in 2020-2021, Tk8.84 in 2021-2022, and Tk11.33 in 2022-2023.

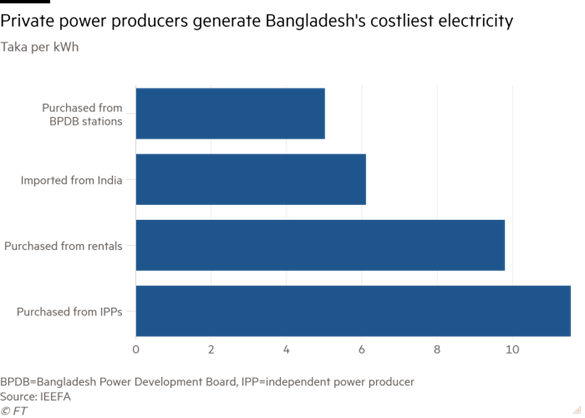

In 2022-23, BPDB’s plants generated power at Tk7.63 per unit, and other state-owned plants at Tk6.85 per unit. In contrast, the average generation cost for independent power producers (IPPs) was Tk14.62, and for rental power plants, it was Tk12.53. A significant portion of the power generation capacity remains unused throughout the year.

However, BPDB, as the sole buyer of power, must pay capacity charges to power plants even if the power is not purchased. Last year, capacity charges exceeded Tk26,000 crore, with 41% of capacity remaining unused.

How is the Rising Electricity Cost Affecting the Public?

The government plans to increase electricity prices quarterly over the next 3 years to remove subsidies from the power sector. Currently, electricity costs Tk7.04 per unit wholesale. This needs to rise to over Tk12 without subsidies. As a result, the average consumer price of Tk8.95 will nearly double to Tk15.

Last year, gas prices rose by 82% on average in January, and electricity prices increased by 5% on average between January and March, contributing to inflation. In March this year, electricity prices rose further from Tk0.34 to Tk0.70 per unit.

Implementing these hikes will undoubtedly increase consumer expenses, especially as higher production costs for electricity-dependent goods will be passed on to consumers. This increase aims to reduce subsidies in the power and energy sectors to meet IMF conditionalities.

Subsidies are necessary because the BPDB buys electricity at high prices from privately owned power plants that use expensive imported liquid fuel. The cost of purchasing power from the private sector is significantly higher than generating power from the public sector.

Each year, as private sector power generation capacity increases, capacity charges and BPDB’s losses also rise. To mitigate these losses, electricity prices have been increased 12 times at the wholesale level and 14 times at the retail level over the last decade and a half.

Bangladesh’s Strategic Shift in Energy Policy

Natural gas emits roughly half the carbon dioxide as coal when burned to produce the same amount of energy. Proponents argue this could enable developing nations to transition away from dirtier fuels like coal and oil while sustaining rapid economic growth.

This proposition appealed to Bangladesh, whose domestic natural gas reserves were insufficient to support a major expansion in power generation. After Prime Minister Sheikh Hasina took office in 2009, the country faced severe electricity shortages.

To address this, her government offered incentives for private companies to build new fossil fuel power plants, including generous capacity payments and legal protections against challenges or prosecution. To rapidly increase supply, Bangladesh also began importing liquefied natural gas (LNG) in 2018.

The strategy proved effective. Bangladesh’s electricity generation capacity soared from 5.5 gigawatts (GW) in 2009 to 23 GW currently, according to the Institute for Energy Economics and Financial Analysis. Consequently, the entire population of 170 million now has access to electricity, compared to less than half in 2009.

Prioritizing natural gas limited the country’s reliance on coal. While coal imports have grown, coal accounts for only 12% of Bangladesh’s generation capacity versus 50% for natural gas. However, electricity demand has not kept pace with the construction boom, resulting in up to 50% excess capacity. Furthermore, the lack of investment in new domestic hydrocarbon exploration means Bangladesh’s natural gas reserves are dwindling.

New liquefaction projects in Qatar, Mozambique, and the US expected to become operational from 2025 onward could ease supply constraints and lower prices by allowing more LNG cargoes to reach global markets.

In conclusion, Bangladesh’s energy sector faces a complex set of challenges as it balances increasing electricity demand, rising generation costs, and the transition to cleaner fuels. Despite substantial investments in gas-fired power plants and the anticipated boost from new gas wells and LNG imports, current supply constraints and infrastructure bottlenecks hinder optimal power generation.

The ongoing capacity payments for underutilized plants exacerbate financial burdens, necessitating frequent electricity price hikes that strain consumers. While the strategic shift towards natural gas has significantly expanded electricity access, the reliance on imported LNG and insufficient domestic gas exploration present long-term sustainability concerns.