Over the past decade, the Western Hemisphere has experienced a profound transformation in the oil industry, emerging as a major player in global oil production. This surge, fueled by technological advancements, market dynamics, and geopolitical factors, has reshaped the energy sectors and holds significant implications for global energy security and economic dynamics.

Historically, oil production had been heavily concentrated in the Eastern Hemisphere, particularly in the Middle East. However, the advent of technological innovations, notably the shale revolution in the United States, has revolutionized the industry. The shale revolution, driven by advancements in horizontal drilling and hydraulic fracturing techniques, has unlocked vast reserves of previously inaccessible oil and propelled the U.S. to the forefront of global oil production.

From 2012 to 2022, Western Hemisphere output surged from 23.0 million barrels per day (27% of the global total) to 31.6 million barrels per day (34% of the global total), according to data from the Energy Institute. This remarkable growth has been further supported by significant contributions from Canada’s oil sands, Brazil’s ultra-deepwater offshore fields, and the emergence of Guyana as a major oil producer.

Drivers of Growth

Shale Revolution in the United States: The U.S. shale boom has been a key driver of Western Hemisphere production growth. Technological advancements in hydraulic fracturing and horizontal drilling have enabled the extraction of oil from previously inaccessible shale formations, leading to a surge in domestic production. The United States surpassed Saudi Arabia as the world’s largest oil producer in 2018, marking a significant milestone in the global oil market. However, recent trends indicate a slowdown in U.S. shale oil growth, with projections suggesting that production growth could be less than half the 900,000 barrels per day (b/d) increase seen at the end of 2023.

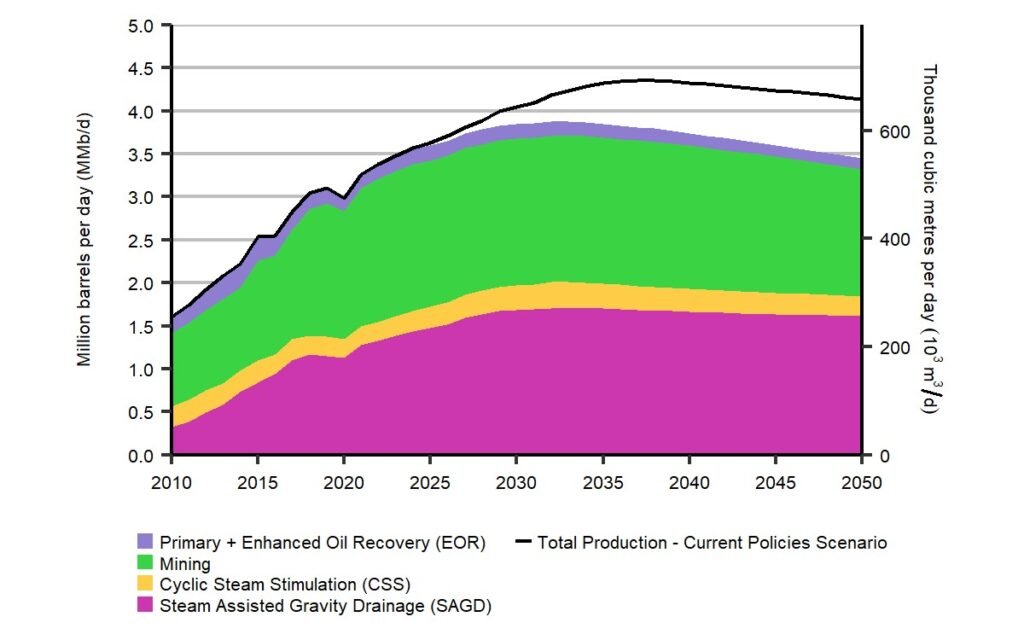

Canada’s Oil Sands: Canada’s vast oil sands reserves have also played a significant role in boosting Western Hemisphere production. Despite challenges such as high production costs and environmental concerns, Canada’s oil sands industry has expanded rapidly, contributing to the region’s overall output growth. Current projections expect Canadian oil sands production to reach 3.5 million barrels per day by 2030.

Brazil’s Offshore Fields: Brazil’s pre-salt offshore fields, located in ultra-deepwater reservoirs beneath thick layers of salt, have attracted significant investment from multinational oil companies. The development of these fields has propelled Brazil into the ranks of major oil-producing nations, further enhancing Western Hemisphere production capacity. Recent plans by Petrobras include the operation of 11 additional FPSO units in the pre-salt layer by 2027, anticipated to boost production significantly.

Emergence of Guyana: The recent emergence of Guyana as a major oil producer has added a new dimension to the hemisphere’s oil landscape. Significant offshore discoveries, particularly in the Stabroek Block operated by ExxonMobil, have positioned Guyana as one of the fastest-growing oil producers in the world. Guyana’s oil production is expected to reach nearly 900,000 b/d by 2025, with further growth anticipated to hit 1 million b/d by 2030.

OPEC’s Role

Despite being dominated by Eastern Hemisphere producers, particularly those in the Middle East, the Organization of the Petroleum Exporting Countries (OPEC) has inadvertently supported the growth of Western Hemisphere production. OPEC’s policies, aimed at curbing production to sustain higher prices, have inadvertently sustained the growth of higher-cost production in the Western Hemisphere, including shale oil in the U.S. and unconventional resources in Canada and Brazil.

By restricting production to keep prices elevated, OPEC has inadvertently provided a lifeline to Western Hemisphere producers, enabling them to thrive in a competitive global market. This paradoxical role highlights the interconnectedness of global oil markets and the complex dynamics that shape production trends.

In recent developments, OPEC and its allies, collectively known as OPEC+, agreed to cut oil production by 1 million barrels per day. This decision has significant implications for global oil markets, potentially benefiting non-OPEC producers like the U.S., Canada, and Brazil by keeping global oil prices at a level that supports their costlier production methods.

The U.S. shale industry, in particular, has demonstrated resilience in the face of OPEC’s influence. U.S. crude oil production reached 13.2 million barrels per day in September 2023, surpassing previous forecasts. The rise in U.S. production has forced OPEC to reconsider its strategies, as it may no longer be able to control prices effectively through production cuts.

Implications for Energy Security

The surge in Western Hemisphere oil production has profound implications for global energy security. As Western Hemisphere producers now contribute significantly to global output, the reliance on Middle Eastern suppliers has lessened. This shift has not only diversified production sources but also reduced geopolitical risks tied to oil supply disruptions, thereby enhancing global energy resilience.

Moreover, the increase in Western Hemisphere production has prompted a reconfiguration of global trade routes. The traditional east-to-west flow of crude oil and refined products is being reversed, transforming energy security. With tanker traffic from the Middle East to Western markets in decline, there is a notable shift in trade patterns. This has geopolitical ramifications, altering the strategic considerations of major oil-importing nations and reshaping the dynamics of global energy geopolitics.

In addition, the global energy crisis has accelerated the transition to cleaner energy technologies, further influencing oil trade flows and energy security. High fossil fuel prices and the push for sustainable energy sources are hastening the move away from reliance on these fuels, which is expected to slow the growth of global oil demand significantly by 2028. This shift towards a clean energy economy is one of the most geopolitically disruptive forces of the 21st century, potentially leading to a peak in global oil demand before the end of this decade.

The surge in Western Hemisphere oil production represents a fundamental shift in global energy dynamics. Fueled by technological innovation, market forces, and geopolitical factors, this transformation underscores the importance of diversifying production sources to ensure stability in the face of geopolitical uncertainties and supply disruptions.

As Western Hemisphere producers continue to assert their dominance in the global oil market, policymakers, industry stakeholders, and consumers must adapt to this new reality to foster a more resilient and sustainable energy future. By embracing innovation, promoting investment, and fostering international cooperation, the Western Hemisphere can play a pivotal role in shaping the future of global energy markets and ensuring a secure and sustainable energy future for all.