Poultry and fish farmers in Bangladesh use digital financial services at significantly higher rates than the other agricultural sector workers.

The adoption of digital financial services (DFS) in Bangladesh has been largely accelerated by poultry and fish farmers, who have adopted these services to improve their financial transactions. These farmers, who comprise a substantial portion of the agricultural workforce, have recognized the benefits of DFS in terms of expediting their financial transactions, enhancing their access to financial services, and boosting their overall productivity.

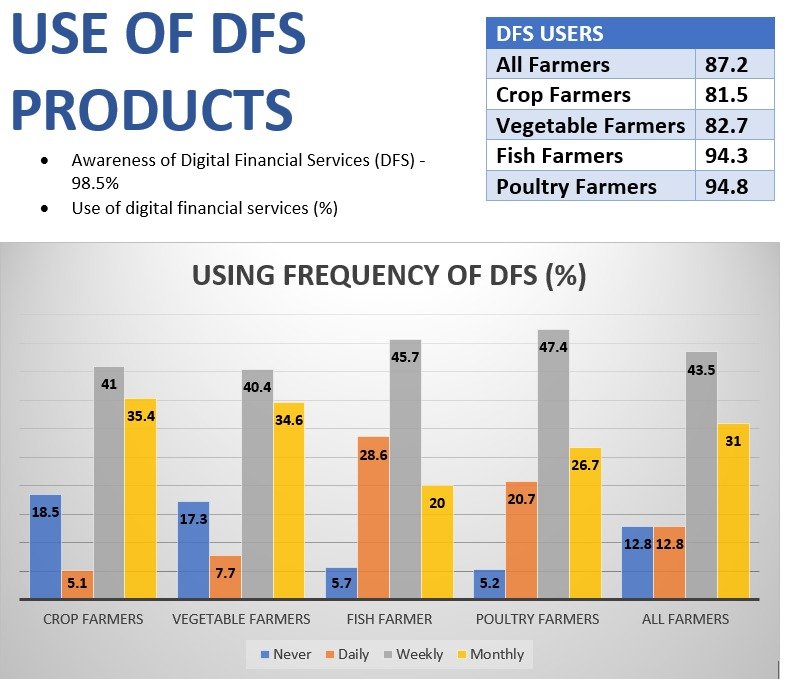

A recent survey conducted by the Policy Research Institute (PRI) with support from the Bill & Melinda Gates Foundation revealed that approximately half of poultry (47.4%) and fish farmers (45.7) in Bangladesh utilize DFS at least once per week. Poultry and fish farmers in Bangladesh have emerged as pioneers in adopting digital financial services, thereby contributing to the expansion of the agricultural sector and empowering marginalized communities.

You can also read: China assures support to Bangladesh in countering power politics, external interference

Adoption of DFS provided farmers options for convenient and secure financial transactions. Ahsan H Mansur, the executive director of PRI, emphasized the significance of financial inclusion in combating poverty and the potential of DFS in bringing the unbanked population into the formal financial system.

The survey conducted by the PRI focused on DFS usage among various marginalized groups, including farmers, indigenous communities, and haor area residents. The findings highlighted the importance of reducing transaction costs for mobile financial services (MFS) in order to increase adoption rates. Three studies commissioned by PRI cast light on the impact and potential of DFS among Bangladesh’s various marginalized groups.

Poultry and fish farmers embrace DFS

Digital financial services have emerged as a game-changer in the agricultural sector, offering numerous benefits to farmers. These services enable secure, convenient, and efficient financial transactions, empowering farmers to manage their finances effectively. Poultry and fish farmers, in particular, have recognized the potential of DFS in enhancing their agricultural activities.

According to the PRI survey, a significant majority of poultry and fish farmers utilize DFS primarily for acquiring essential resources such as feed, chick/egg/fingerlings, and medicine/insecticide. Additionally, they also utilize DFS to receive payments for their products.

Chicken (94.8%) and fish (94.3%) farmers are more likely to utilize MFS/DFS, as among other farmers, poultry, and fish farmers are a little richer, more educated, younger, and more technologically advanced, the study revealed.

One of the research papers presented at the national consultation discussed the adoption. The study found that bKash is the most popular DFS product among farmers, followed by Nagad and Rocket. According to the report, Bkash (82%) is the most popular among respondents, followed by Nagad (30%) and Rocket (23%).

However, because the payment amount is minimal and transaction fees are cheap, DFS is most typically used for utility bill payments. Moreover, farmers still prefer cash transactions to minimize risks associated with large sums of money.

Challenges in building financial resilience for indigenous communities

Another study focused on providing digital financial services to plain land indigenous communities in northern Bangladesh, such as the Santal and Orao groups. According to the findings, a significant proportion of respondents from these communities’ own mobile phones, but MFS usage is comparatively low.

Lack of digital literacy, limited access to mobile, and lack of electricity have been identified as obstacles to the adoption of DFS. 27% of respondents lack knowledge and understanding of MFS. The majority of MFS users receive SSNP transfer payments, remittances, and utility bill payments. Although the overwhelming majority (84%) of MFS accounts were opened with the assistance of MFS agents, only 42% are currently utilized.

The respondents’ illiteracy or lack of formal education is another significant reason for their inability to use MFSs. Only 35% of respondents completed secondary school, and respondents with higher levels of education are more likely to use MFS.

Moreover, the percentage of women who own a mobile phone is even lower (31%). 75% of masculine respondents actively use MFSs, whereas only 25% of female respondents do so. In terms of mobile phone ownership and usage, women from these communities confront additional challenges.

DFS for poverty alleviation: Insights from the Haor study

The third study examined the impact of DFS on poverty among Bangladeshi haor inhabitants and the potential of DFS to improve the lives and livelihoods of the haor population. The majority of respondents were aware of DFS and owned bank accounts, according to the research. However, relatively few payments and transactions were conducted using DFS.

The study found that 65.66% of Haor area respondents had bank accounts and 64.66% had accounts with NGOs.

The majority of respondents (81.33%) were aware of or knowledgeable about MFS/DFS. 52.37% of respondents with MFS/DFS knowledge owned and independently used their accounts, while 45.65% used their accounts with assistance from others and 1.99% did not have their own accounts and used those of others.

In the first utilization scenario of MFS/DFS, 68.30% of respondents received money, 17.04% sent money, and 11.2% received social safety net program benefits, according to the study. The majority of respondents (69.37%) had MFS/DFS retail agent outlets within two kilometers of their residences.

What could be done to increase DFS usage among farmers?

The findings of these studies highlight the need for policymakers and stakeholders to resolve the obstacles preventing marginalized groups from adopting DFS. Key challenges such as complexity of transactions (25.39%), unavailability of mobile phones (14.87%), lack of guidance on MFS/DFS usage (13.42%), unavailability of electricity (12.69%), and absence of a photo (10.70%) were identified as obstacles to DFS adoption.

Among the farmers, around 18.5% of the crop farmers and 17.3% of vegetable farmers have never used DFS in their life. To increase farmers’ digital financial literacy in Bangladesh, targeted awareness and education programs must be implemented. These programs should include comprehensive training on digital financial services, including mobile banking and wallets. Through collaboration with agricultural extension services and organizations, existing farmer training programs can be augmented with digital financial literacy training.

Increasing access to affordable smartphones through partnerships with manufacturers and service providers is essential. Through collaboration with NGOs and microfinance institutions, their programs can incorporate digital financial literacy. Increasing the number of digital service agents in rural areas allows for the provision of individualized assistance. By implementing these strategies, farmers can acquire the knowledge and skills necessary to utilize digital financial services effectively, enabling them to access a broader array of financial services and contribute to their economic growth.

To further promote DFS, recommendations include reducing transaction costs and improving network infrastructure in rural areas.

Lastly, the adoption of DFS by poultry and fish farmers in Bangladesh can increase financial inclusion and empower marginalized populations, but obstacles such as transaction costs and limited access to technology must be addressed for widespread implementation and enhanced impact among all the farmers.